More than half of Filipino adults don’t have enough savings to handle an emergency, according to the Bangko Sentral ng Pilipinas. That’s not just a statistic, that’s families worrying about how to pay for the next hospital bill, repair a roof after a typhoon, or survive a sudden job loss. In the Philippines, where natural disasters are part of life and medical costs can escalate quickly, building an emergency fund isn’t optional. It’s protection. It’s peace of mind. It’s the difference between a temporary setback and long-term debt.

An emergency fund should ideally cover 3–6 months of essential living expenses, enough to keep food on the table and the lights on if income suddenly stops. Without it, many people end up relying on loans or their credit card just to stay afloat. The good news? There’s never been a better time to start. With digital banks offering competitive rates, you can grow your savings faster through a smart high interest savings account comparison and by understanding safe short term investment options. In this guide, we’ll walk through how much to save, where to store it, and how to build it step by step, in a way that feels realistic, not overwhelming.

What is an Emergency Fund and Why Do You Need One?

Think of your emergency fund as your financial “shock absorber.” It’s money set aside strictly for unexpected, necessary, and urgent expenses. Not for vacations. Not for a new phone. Not for investment opportunities that “look promising.”

It exists for the moments you didn’t plan for, but that life eventually brings.

Real Emergencies Filipinos Face

If you live in the Philippines, you already know how unpredictable things can be.

- A parent suddenly confined in the hospital, even with PhilHealth coverage.

- A freelance contract that isn’t renewed.

- Flood damage after days of heavy rain.

- An urgent flight home for a family emergency.

Without savings, these situations often lead to borrowing, and that’s where interest charges start compounding stress.

The 3–6 Month Rule Explained

Financial planners typically recommend:

- Single earners: At least 3 months of expenses

- Families with dependents: 6 months

- Freelancers or self-employed: 6–12 months

The more unstable your income, the bigger your safety net should be. It’s not about fear, it’s about preparation.

Emergency Fund vs. Savings vs. Investments

Emergency funds are not designed to earn the highest returns. They’re designed to be there when you need them.

Before withdrawing, ask yourself:

Is this unexpected, necessary, and urgent?

If the answer is no, it probably isn’t an emergency.

How to Calculate Your Emergency Fund Target

The Essential Expenses Method

Start with the basics, what you absolutely need to survive:

- Rent or mortgage

- Utilities

- Groceries (not dining out)

- Transportation to work

- Medications or insurance premiums

- Minimum debt payments

- Phone and internet

Remove wants. Strip it down to survival mode.

Sample Scenarios

- Single professional in Manila:

₱25,000 × 3 months = ₱75,000 - Family of four in Cebu:

₱45,000 × 6 months = ₱270,000 - Freelancer in Davao:

₱30,000 × 6 months = ₱180,000

These numbers may feel big. That’s normal. You’re not building it overnight, you’re building it consistently.

Adjusting for Your Situation

- Dual-income household? You may aim for the lower end.

- Single breadwinner? Aim higher.

- Government employee with stable tenure? Slightly lower cushion may work.

- Commission-based earner? Prepare for volatility.

The goal isn’t perfection. The goal is preparedness.

Where to Store Your Emergency Fund: The Storage Hierarchy

Your emergency fund doesn’t need to sit in just one account. Think in layers.

Tier 1: Immediate Access (1 Month)

Keep one month of expenses in a traditional bank savings account with ATM access.

Examples include:

- BDO

- BPI

- Metrobank

The interest rates are low, but access is instant, and that’s what matters here.

Tier 2: High-Interest Digital Savings (2–4 Months)

For the rest, digital banks can help your money grow faster.

Options include:

- Maya Bank

- Tonik Bank

- GoTyme Bank

- UNO Digital Bank

Rates can range from 3% upward depending on conditions. Withdrawals may take a day or two, acceptable for non-immediate emergencies.

Tier 3: Short-Term Growth (Beyond Core Fund)

Once your full 6 months is complete, you can consider low-risk growth options like:

- 30–90 day time deposits

- Money market funds

But remember: Accessibility matters more than returns.

High-Interest Savings Account Comparison 2025

Doing a proper high interest savings account comparison ensures your money isn’t just sitting, it’s quietly working.

Short-Term Investment Options for Excess Emergency Funds

Only consider these after completing at least six months of expenses.

Money Market Funds

Offered by platforms like:

- COL Financial

They invest in short-term debt instruments and typically allow redemption within 2–3 business days.

Short-Term Time Deposits

Digital banks often offer 30–90 day terms with competitive rates. A laddering strategy can maintain liquidity.

Government Securities

Retail Treasury Bonds are government-backed but less liquid.

Avoid stocks, crypto, and volatile assets. Emergency funds should not fluctuate dramatically.

Building Your Emergency Fund: Actionable Strategies

Pay Yourself First

Automate your savings the moment income arrives.

Income – Savings = Expenses.

Adjust the 50-30-20 Rule

In the Filipino context, flexibility matters. Family obligations are real. Adjust, but prioritize your emergency fund.

Accelerate Growth

- Save your 13th month pay

- Use bonuses wisely

- Try a no-spend month

- Monetize a skill

Even ₱500 per week equals ₱26,000 a year.

Real Story: Candice’s 12-Month Safety Net

Candice, a freelance graphic designer earning around ₱30,000 monthly, used to feel anxious every time a project ended. Instead of waiting for a “better” month, she automated ₱5,000 into a digital bank account every time she got paid. She treated it like rent, non-negotiable.

Twelve months later, she had ₱60,000 saved. When two clients paused their contracts for nearly two months, she didn’t panic. She didn’t reach for her credit card. Her emergency fund covered rent and groceries while she searched for new work. What changed wasn’t just her bank balance, it was her confidence.

Consistency beats income.

When to Use (and Replenish) Your Emergency Fund

Legitimate Uses

- Medical emergencies

- Job loss

- Essential repairs

- Urgent family crisis

Not Emergencies

- Travel deals

- Gadget upgrades

- Investment opportunities

If you use it, rebuild it. Pause other goals. Focus on replenishment within 6–12 months.

Conclusion

Creating an emergency fund in the Philippines is one of the most empowering financial decisions you can make. It gives you breathing room. It protects your dignity. It keeps you from turning to high-interest debt or maxing out your credit card when life becomes unpredictable.

You don’t need to start big. ₱1,000 today is better than ₱0. What matters is the system, choosing the right account, automating your savings, and staying consistent. If you’re unsure where to begin, platforms like Finmerkado can help you compare savings accounts and financial tools so you can make informed decisions.

The best time to start was yesterday. The second-best time is today.

Frequently Asked Questions

Most financial experts recommend saving 3–6 months of essential living expenses. If you’re single with stable employment, three months may be enough. If you have dependents, are self-employed, or earn irregular income, aim for six months or more. The key is calculating your essential monthly expenses — not your full lifestyle budget — and multiplying that amount accordingly.

Your emergency fund should be kept in a safe, liquid, and accessible account. Many Filipinos now use digital banks offering higher rates than traditional banks. Options like Maya Bank, Tonik Bank, GoTyme Bank, and UNO Digital Bank provide competitive interest while maintaining accessibility. The priority is liquidity — not maximum returns.

Your core emergency fund should not be invested in stocks, cryptocurrency, or volatile assets. However, once you’ve completed at least six months of expenses, you may consider low-risk short term investment options Philippines such as time deposits or money market funds for excess funds. Accessibility and capital protection should always come first.

A credit card can help in temporary cash flow gaps, but it should not replace an emergency fund. Interest charges can accumulate quickly if balances aren’t paid in full. An emergency fund prevents you from relying on debt and protects your financial stability during unexpected situations.

A true emergency is unexpected, necessary, and urgent — such as medical bills, job loss, essential home repairs, or sudden family crises. Travel deals, gadget upgrades, and investment opportunities do not qualify. If the expense can wait or be planned for, it should not come from your emergency fund.

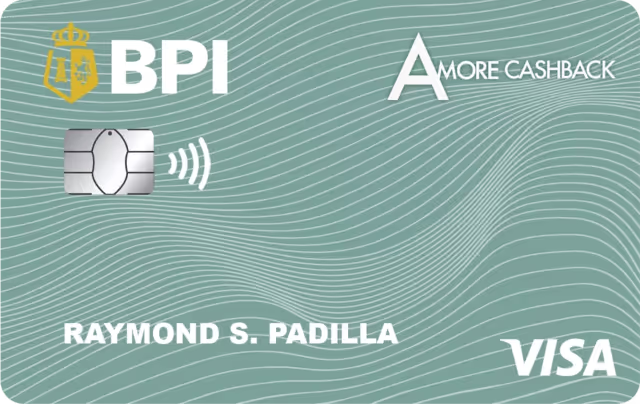

BPI Amore Cashback Card

- Get up to 4% cash back on supermarkets and department store spend

- Get up to 1% cash back on drugstore and bills payment spend

- Earn up to 0.3% cash back on all other local retail spend

- Enjoy unlimited access exclusive customer and family lounges in Ayala Malls

- One of the lowest forex conversion rates at 1.85%

- Ideal for cardholders who love saving while shopping

Petron BPI Card

- Earn 3% rebate on fuel

- Free ₱200 fuel voucher for first-time cardholders

- Avail of flexible and convenient installment plans

- Convert your credit limit to cash for emergencies

- Ideal for car owners

RCBC Classic Mastercard

- Earn flexible non-expiring Rewards Points from all your purchases

- Convert your points to air miles and other rewards

- Free budget monitoring tools

- Convert straight purchases made anywhere to installment

- Free travel insurance and purchase protection

- No Annual Fee For Life

- Ideal for the young professionals enjoying financial independence

BPI Personal Loan

Need a cash boost for life’s big moments or unexpected emergencies? The BPI Personal Loan offers a reliable and flexible solution—whether you’re funding a small business, covering tuition, or consolidating debt. With competitive rates, fixed monthly payments, and a fast approval process, this loan is designed to fit your goals and your lifestyle. No collateral required, just straightforward access to funds when you need them most.

Chinabank Personal Loan

Chinabank’s Easi‑Funds Personal Loan (via China Bank Savings) offers unsecured financing of up to ₱1 million, positioned similarly to peer offerings. It carries an add‑on interest rate of approximately 1.3%–1.5% monthly, translating to an estimated APR of 16%–19% depending on loan tenure and credit profile. Tenure options generally range from 12 to 36 months, while approval often comes within 3 to 5 banking days. Being backed by Chinabank’s extensive branch network and digital infrastructure, it combines legacy banking strength with modern convenience.

EastWest Personal Loan

Unsecured personal loan designed for flexible multi-purpose use—whether for tuition, travel, or business needs. Offers terms up to 60 months and competitive add-on rates.