Starting a negosyo in 2025 is both simpler and trickier: payments and delivery are easier, but costs remain high and customers expect speed. The right move is a business you can test in weeks, not months, with cash flow that pays for itself early. If you already maintain disciplined spending through a rewards card, consider channeling pilot expenses through a responsible credit line to track costs and earn rebates—use this carefully and compare terms on your bank’s page once you’ve fixed a budget. As Ramon Magsaysay said, “Those who have less in life should have more in law;” in business, those who prepare more on paper risk less in practice.

This guide prioritizes ideas you can validate quickly, with lean tools and clear unit economics. It also reframes the sari‑sari store as a modern micro‑distribution hub, not just a shelf of snacks.

2025 Landscape for Starting a Small Business

Inflation has cooled from peaks but remains sticky for food and transport. Policy rates are easing, yet bank credit screens for stable cash flow. Households are mixing salaried work with side gigs, making time and predictability real constraints. Your edge is speed: launch a narrow offer, learn fast, keep records.

- Demand is online‑first and hyperlocal. Customers discover on Facebook, TikTok, or marketplaces, but expect neighborhood‑level fulfillment.

- Labor is flexible. Students and part‑timers can cover peak hours; build schedules around demand spikes.

- Compliance is manageable if you focus on basics: business name and barangay/Mayor’s permit where applicable; keep receipts and a simple ledger.

Subtle note: For pilots that require a small float (packaging, first inventory), some entrepreneurs use a low‑fee card with category rewards and pay in full each cycle to avoid interest. If you explore this path, do it with a capped budget and compare options on your credit card resource before committing.

How to Choose the Right Idea - A Quick Framework

- Fit: skills, time window, and starting capital. If you can only spare evenings and weekends, prefer delivery‑friendly or appointment‑based services.

- Demand: evidence from search/social threads, marketplace rankings, and local groups. Count comments and actual orders, not likes.

- Unit economics: price minus direct costs (COGS and delivery) should leave a contribution margin that funds overhead and payback within 1–3 months.

Table 1 — Unit economics mini‑check (example)

If your monthly overhead (data, utilities, tools) is ₱3,000, you need ~30 orders to break even. Make the first target tangible: 10 orders per week.

Low‑Capital, Home‑Based Business Ideas (Validated for 2025)

- Food kits and niche “ready‑to‑heat”

- Lean menu: one hero item, two variants, weekly pre‑orders.

- Edge: predictable batches reduce waste and protect margins.

- Test: 50 sample boxes to neighbors and condo groups; collect reviews with photos.

- Services with simple gear

- Cleaning/detailing, appliance checks, tutoring, at‑home beauty.

- Pricing ladder: “basic,” “plus,” “subscription” to lift average order value.

- Calendar: open peak slots (Sat/Sun mornings, weekday evenings). Use free booking links.

- Digital micro‑products

- Templates, checklists, neighborhood guides; bundle with a short video.

- Distribution: Facebook Groups + GCash/PayPal payment links.

- IP basics: original content; use clear usage terms in your product page.

Practical anchor: For procurement or recurring software fees, many founders separate personal and business expenses using a dedicated card to simplify bookkeeping. If you’re comparing options, review terms and fees on your credit card guide and stick to a “pay‑in‑full” rule.

Small Business Ideas for Students and Part‑Timers

- Campus or barangay pre‑order reselling

- Collect orders Mon–Wed, fulfill Fri–Sat to minimize leftover stock.

- Rotate themes: stationery week, tech accessories week, review week.

- Social media micro‑agency for local MSMEs

- Offer content shoots + scheduling + quarterly promo calendar.

- Price by bundle, not hourly; include one revision cycle.

- Study‑adjacent gigs

- Note summaries, language tutoring, lab support with proper approvals.

- Keep clear deliverables and deadlines; request testimonials to build proof.

Rethinking the Sari‑sari Store: From Shelf to Micro‑Hub

A sari‑sari store can be more than retail. It can be a neighborhood micro‑distribution center with higher turnover items and services:

- Inventory strategy: track top 50 items; expand only those that hit target velocity.

- Services: e‑load, bills payment, parcel drop‑off/pick‑up, water-refill tokens.

- Pre‑order wall: collect orders for fresh items (bread, produce) with fixed pickup times.

- Data habit: weekly stock count of fast movers; cut SKUs that sit.

- Forward move: partner with home bakers or farmers for consignment; store takes a fair cut for shelf and promo.

Table 2 — Micro‑hub SKU policy (example)

Food Business Ideas — Costs, Compliance, Quick Tests

- Kitchen standards: clean prep area, labeled containers, temperature control for perishables.

- Permits: check LGU guidance for home‑based food sellers; some require inspection for larger volumes.

- Cost control: portion scoops, supplier discounts for batch orders, standard recipes to reduce variance.

- Two‑week pilot:

- Week 1 — MVP menu, friends‑and‑neighbors test, collect feedback.

- Week 2 — Open to two nearby streets/condo towers; cap orders to protect quality; track returns and complaints.

Funding a Small Business Without Heavy Risk

- Bootstrapping first: customer pre‑orders, deposits for customized items, and small “founding batch” discounts.

- When small loans make sense: equipment with clear ROI (e.g., freezer, mixer) or consolidating costly revolving credit into a predictable amortization. Map cash flow before borrowing.

- Lender view: predictable margins and documented orders matter more than slides. Keep a simple ledger, screenshots of orders, and supplier invoices.

Subtle anchor: If you’re evaluating whether a starter card or a small personal loan can smooth cash flow, study total cost and repayment schedule on your loans page before applying. Use credit to bridge timing, not to cover a weak model.

Tools and Software to Run Lean

- Payments: QRPH/GCash/PayMaya links; issue simple e‑receipts.

- Inventory and orders: a shared Google Sheet with reorder triggers; free kanban boards for job status.

- Messaging: canned responses for FAQs; response‑time targets.

- Forecasting: a one‑page cash‑flow file—expected orders, COGS, delivery spend, overhead, and next week’s purchase plan.

Weekly habit: 30‑minute “numbers review.” Check orders, contribution margin, repeat rate, and cash runway. Adjust menu, pricing, or promos based on those four metrics alone.

One‑Page Launch Checklist

- Validate demand with a pre‑order post and five paid test customers.

- Register basics (BN/DTI/LGU as required); open a dedicated wallet or account.

- Set prices from unit economics, not competitors’ guesses.

- Prepare a refund and complaints script—trust grows when you fix mistakes fast.

- Collect reviews from the first 20 buyers; secure permission to reuse photos.

- Schedule the first “rest day” for admin and stock count—businesses burn out without one.

FAQs (2025 quick answers)

- What’s the cheapest small business to start at home?

Services or pre‑order food kits. Minimal equipment, quick validation, and predictable batches. - How much capital for a simple food stall?

Varies by equipment and location, but pilot from home first. Prove 50+ weekly orders before paying for rent. - Are student‑run businesses allowed without a full permit? Check campus and LGU policies. Keep volumes small while testing; register once you operate regularly.

Conclusion

Build Small, Learn Fast, Scale What Works

Opportunity in 2025 belongs to founders who respect numbers and time. Start with a narrow offer, keep receipts, and watch contribution margins like a hawk. Use tools that lower friction and documentation that earns trust. Platforms like Finmerkado can also help you stay financially organized—whether you’re comparing business credit options, tracking costs, or planning cash flow. A modern sari-sari mindset—serving needs quickly and locally—will win more than a flashy launch. As Peter Drucker noted, “What gets measured gets managed.” Measure early, manage calmly, and let momentum do the heavy lifting.

Frequently Asked Questions

Validated low‑capital options include pre‑order food kits, home‑based services (cleaning, tutoring, beauty), and digital micro‑products (templates, guides). Choose ideas with fast validation and clear unit economics.

Evaluate Fit (skills/time/capital), Demand (evidence from marketplaces and local groups), and Unit Economics (price – COGS – delivery – platform fees). Target a 1–3 month payback and track contribution margin per order.

Use pre‑order reselling cycles, simple service bundles for SMEs (content + scheduling), or study‑adjacent gigs. Limit fulfillment to peak windows and collect testimonials to build social proof.

Turn it into a micro‑distribution hub: focus on fast‑moving SKUs, add e‑load/bills payment/parcel services, and run pre‑orders for fresh goods. Track weekly turns and discontinue slow movers or convert them to pre‑order only.

A narrow ready‑to‑heat menu with weekly batches. One hero item keeps COGS predictable and reduces waste. Use a two‑week pilot with capped orders and documented feedback.

Costs vary by equipment and location; pilot from home first. Prove consistent 50+ weekly orders and positive contribution margins before committing to rent or a kiosk.

Bootstrap first with pre‑orders. If using credit, choose a low‑fee card or a small, predictable loan only after mapping cash flow and total cost. Separate business and personal expenses, pay cards in full each cycle, and keep DTI healthy before borrowing.

Payment links (QRPH/GCash/PayMaya), a shared inventory/order sheet with reorder triggers, a free kanban board for job status, canned message replies, and a one‑page cash‑flow forecast updated weekly.

Check LGU rules for home food operations; many require barangay clearance and Mayor’s permit at certain volumes. Keep receipts and a simple ledger for taxes and lender reviews.

Orders, contribution margin per order, repeat rate, and cash runway. Use these to adjust pricing, menu, inventory, or promo spend.

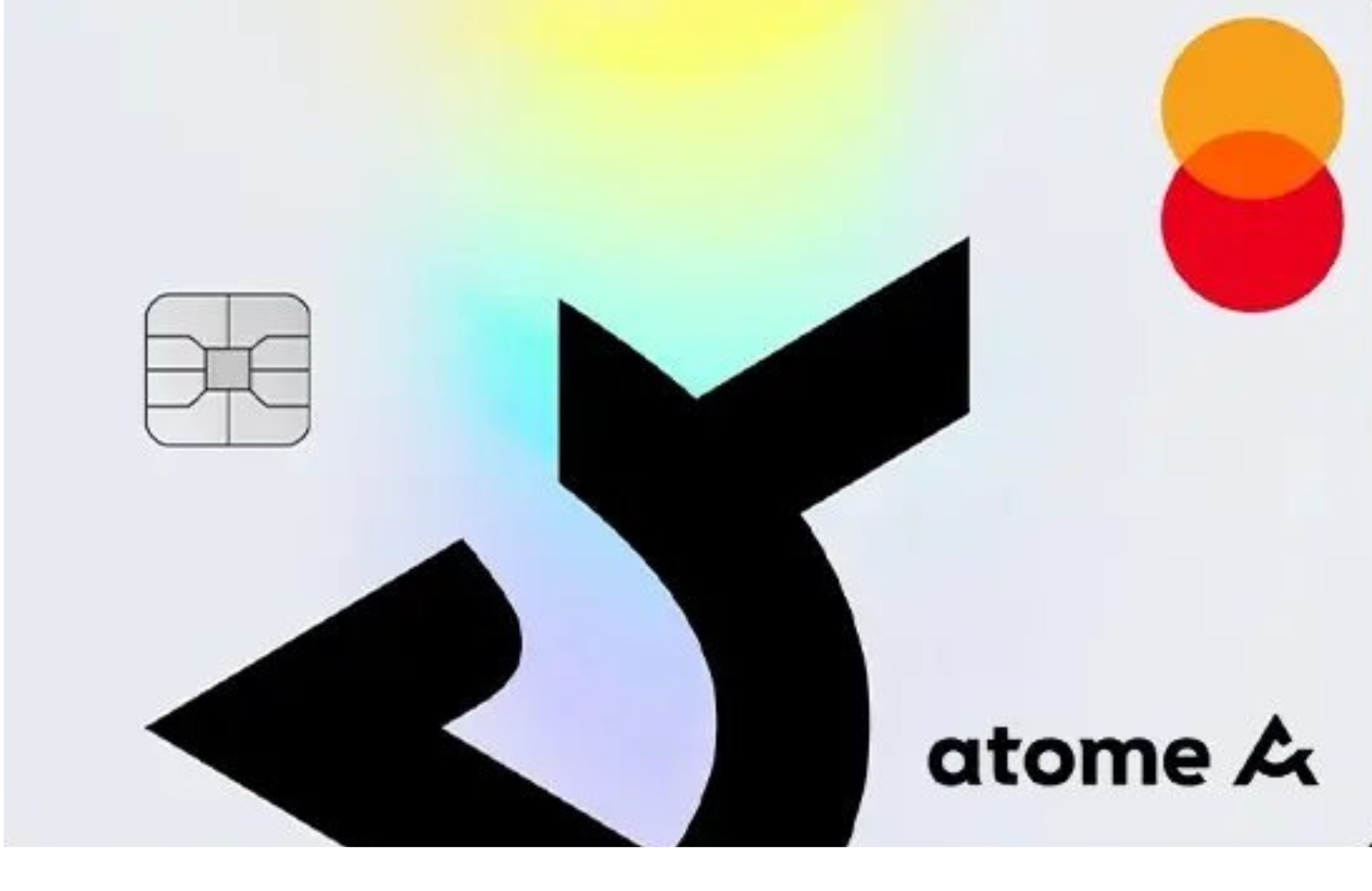

Atome Card

- Buy Now, Pay Later (BNPL) Card

- Up to ₱200,000 spending limit

- Pay later at 0% interest for up to 40 days

- Flexible installment plans up to 6 months

- No annual fees, hidden charges and tedious paperwork

- Fast online application in under 90 seconds

Metrobank Toyota Mastercard

- 3% fuel rebate at Petron, up to a total annual cap of ₱15,000

- 10% discount on parts, accessories, and labor at Toyota dealerships

- Double Rewards Points: Earn 2× points (₱20 spend = 1 point) at your preferred Toyota dealer

- Flexible financing perks: 0% installment plans for services at authorized Toyota dealers, and travel insurance & roadside assistance

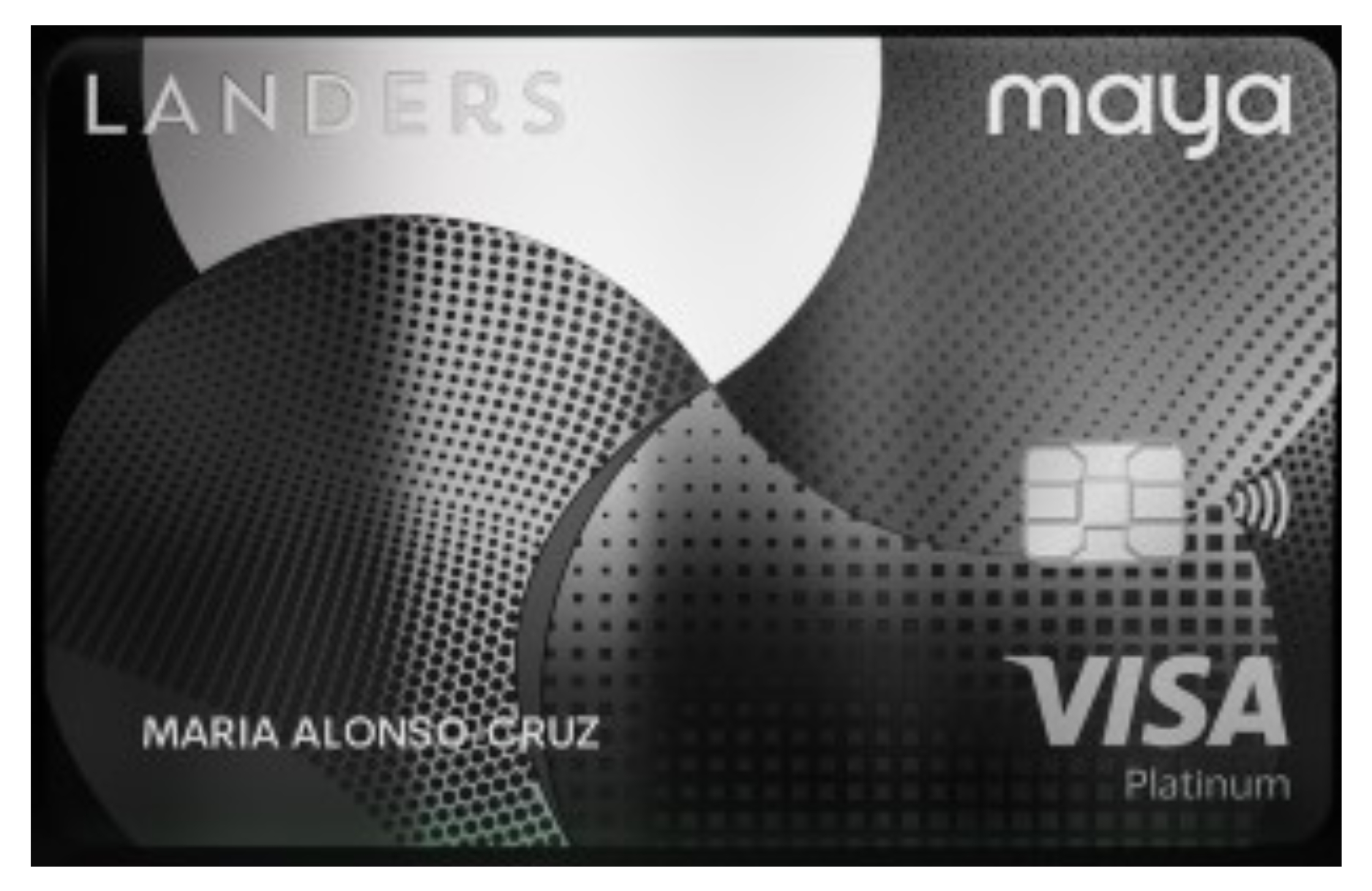

Maya Landers Cashback Credit Card

- No annual fee with just one monthly transaction

- Earn up to 5% cashback at Landers on in-store and online purchases

- Get 2% cashback on dining and 1% cashback on other local or international spends.

- Exclusive Landers perks—enjoy discounts, promos, and store access with your membership.

- Complete in-app control—freeze/unfreeze, view transactions, manage limits, and redeem cashback instantly.

BDO Unibank Personal Loan

BDO Unibank’s Personal Loan offers unsecured financing of up to ₱2 million with a fully digital or branch-assisted application process. It’s an accessible cash option for immediate needs like debt consolidation, travel, events, and other lifestyle expenses. With competitive rates starting at 0.98% monthly add-on and flexible repayment up to 36 months, it’s a solid choice for salaried and self-employed individuals.

BPI Personal Loan

Need a cash boost for life’s big moments or unexpected emergencies? The BPI Personal Loan offers a reliable and flexible solution—whether you’re funding a small business, covering tuition, or consolidating debt. With competitive rates, fixed monthly payments, and a fast approval process, this loan is designed to fit your goals and your lifestyle. No collateral required, just straightforward access to funds when you need them most.

Maya Personal Loan

Want a personal loan that’s 100% mobile and super convenient? The Maya Personal Loan is built for the digital lifestyle, no paperwork, no long lines. With just your Maya app, you can apply, get approved, and manage your loan. Whether it’s for bills, tuition, or a financial cushion, Maya’s fully digital loan service puts speed and flexibility right in your hands.